When you begin to compare pet insurance plans online, the process often feels like walking into a giant room full of colorful boxes. Every box promises something exciting—“best value,” “full coverage,” “customer favorite”—but the inside of each box feels different once you open it. Some are light. Some are heavy. Some hide small rules in the corners. Yet in the end, you only want one thing: a plan that protects your pet without confusing you or hurting your budget.

This guide walks you step-by-step through everything you need to compare plans clearly.

No complicated words.

No insurance-style paragraphs.

Just simple, visual explanations that help you understand each part the moment you read it.

If someone ever asks you how to compare pet insurance plans, this is the guide you will wish you always had.

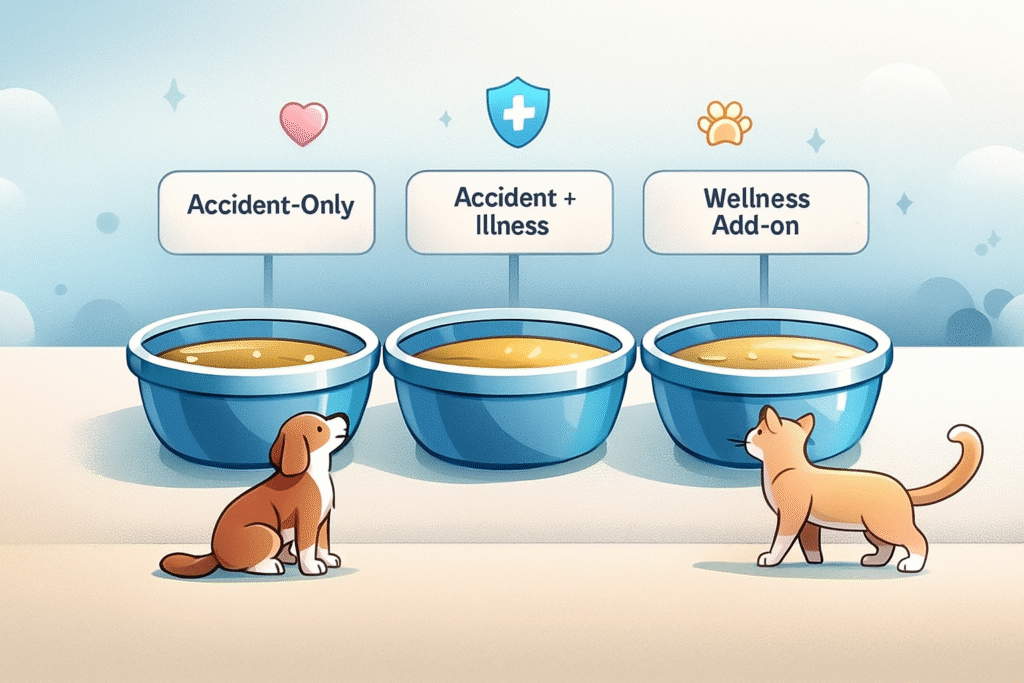

Step 1: Know the Plan Types

Before comparing anything—price, benefits, reimbursement—you must know what type of plan you’re actually looking at. Without this, every plan looks similar, even though they behave differently in real life.

Imagine three water tanks lined up:

- The first tank fills halfway.

- The second tank fills fully.

- The third overflows.

These tanks represent the three types of pet insurance.

Accident-Only (Half-Full Tank)

This plan protects against sudden injuries—fractures, bites, accidents, cuts. It’s basic and cheap. If your pet is energetic, jumps high, or runs fast, this tank is your emergency shield. But it does not protect against sickness.

Accident + Illness (Full Tank)

This is the plan most pet owners choose in any pet insurance comparison.

Why? Because most vet bills come from illness, not accidents.

It covers:

- Fever

- Infections

- Long-term diseases

- Skin issues

- Stomach problems

- Breed-related risks

- Surgeries

This is the tank that supports you every time your pet shows symptoms you didn’t expect.

Wellness Add-ons (Overflow Tank)

Some pets need regular care—dental cleaning, vaccinations, flea control, check-ups.

A wellness add-on makes your yearly vet routine smoother. But not all wellness plans are priced fairly, so comparing them matters.

When you understand these tanks, you begin comparing with clarity instead of confusion.

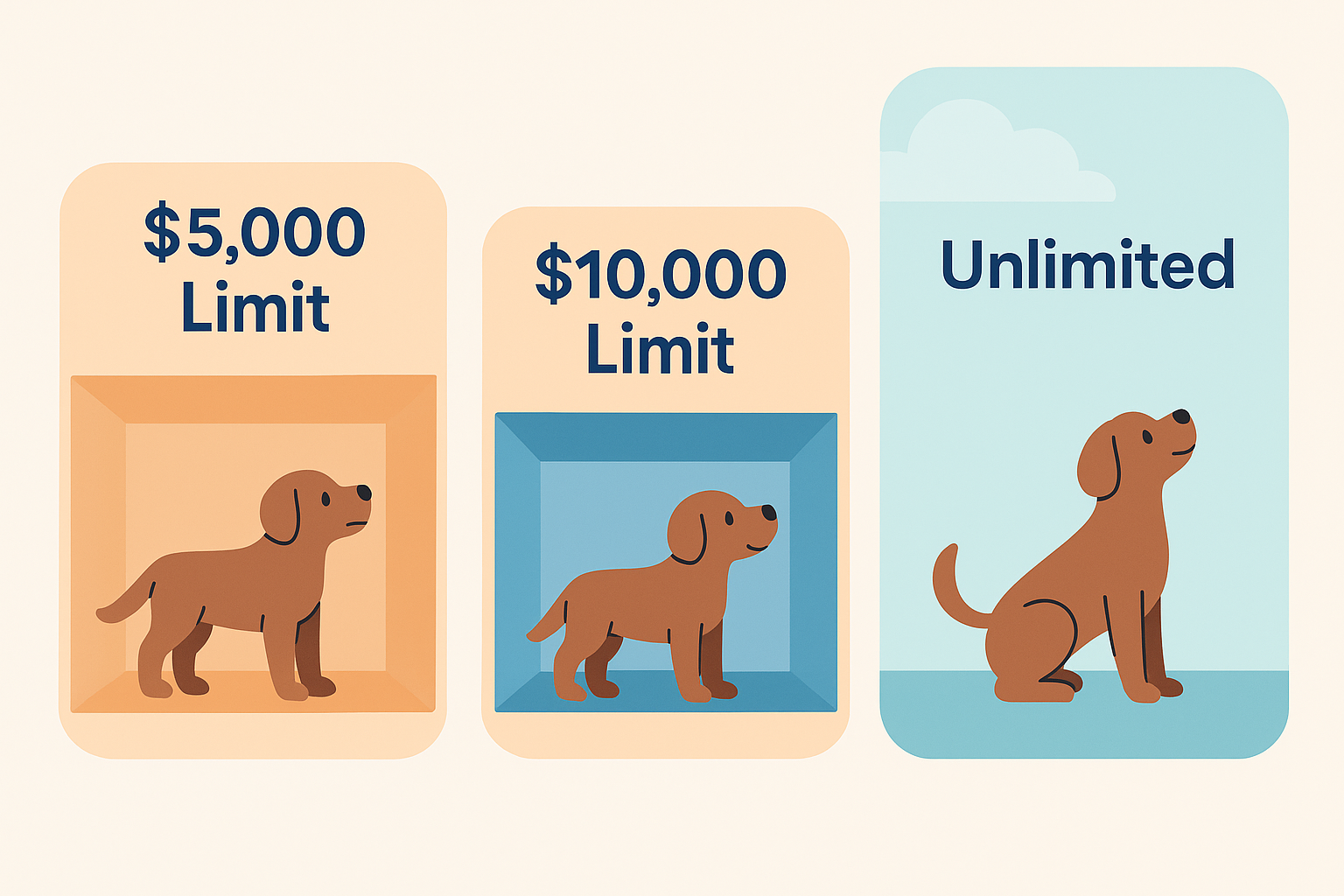

Step 2: Compare Annual Limits

Annual limits are the roofs above your pet.

A low roof makes you bump your head.

A high roof lets you breathe comfortably.

And no roof means the sky’s open.

Typical limits include:

- $5,000 (₹4,15,000)

- $10,000 (₹8,30,000)

- Unlimited

A single emergency surgery often costs $2,000–$4,000 (₹1,66,000–₹3,32,000).

So choosing the right roof matters more than people think.

Table: Best Limits Based on Pet Personality

| Pet Personality | Best Limit | Why |

|---|---|---|

| Calm indoor pet | $5,000 (₹4,15,000) | Low emergency risk |

| Curious explorer | $10,000 (₹8,30,000) | More chances of accidents |

| High-risk breed | Unlimited | Conditions repeat or worsen |

Most people choose limits by price.

But your pet’s personality is often more accurate than age or breed alone.

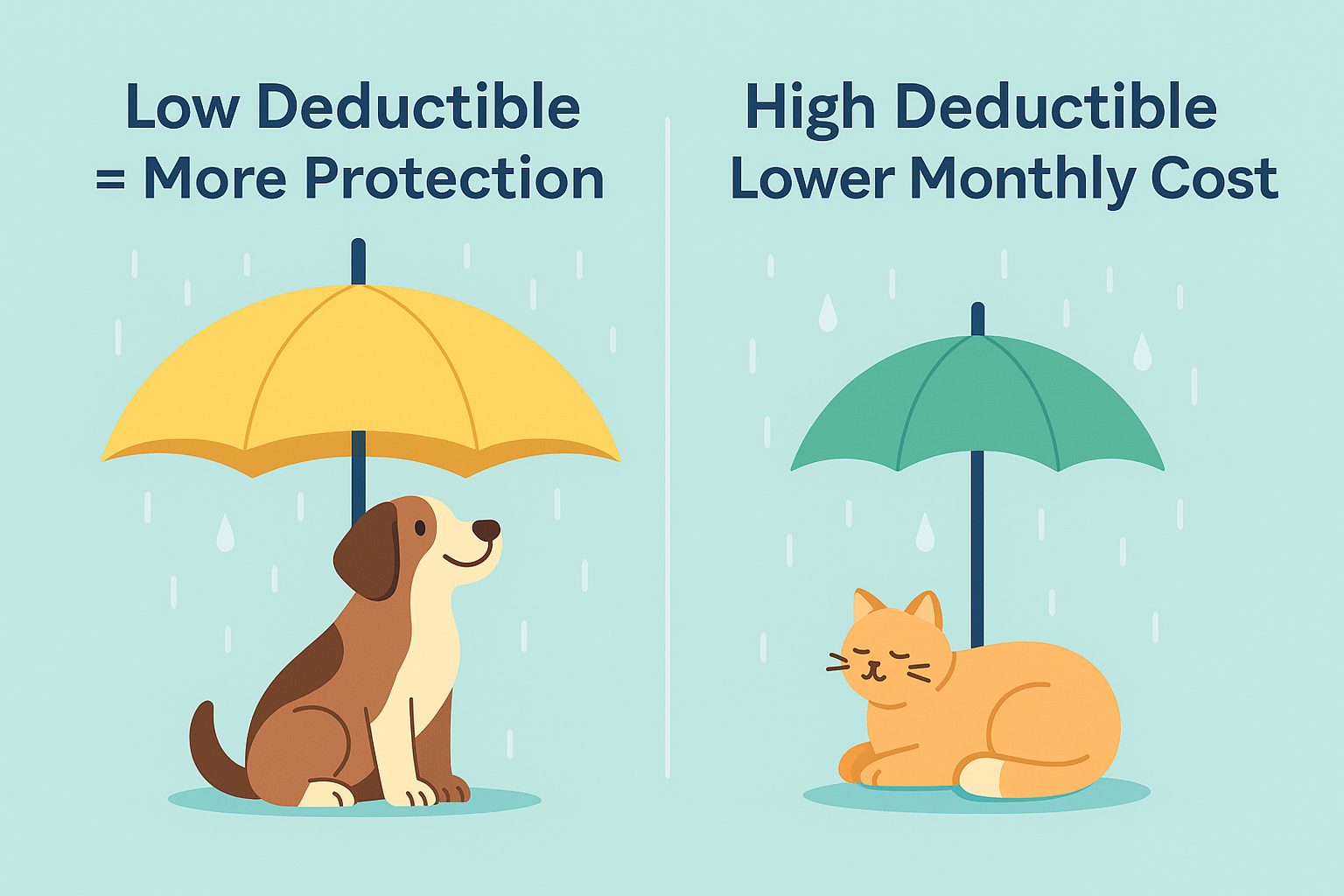

Step 3: Compare Deductibles

A deductible is the amount you pay before insurance steps in.

Think of it as the first stone you must move before help arrives.

Common deductibles include:

- $100 (₹8,300)

- $250 (₹20,700)

- $500 (₹41,500)

- $1,000 (₹83,000)

Higher deductible → cheaper monthly premiums

Lower deductible → higher monthly premiums but less stress during claims

Many think deductibles are about money.

But they’re actually about comfort.

If sudden bills scare you → choose a lower deductible.

If monthly savings matter → choose a higher deductible.

This emotional balance is rarely talked about but deeply important.

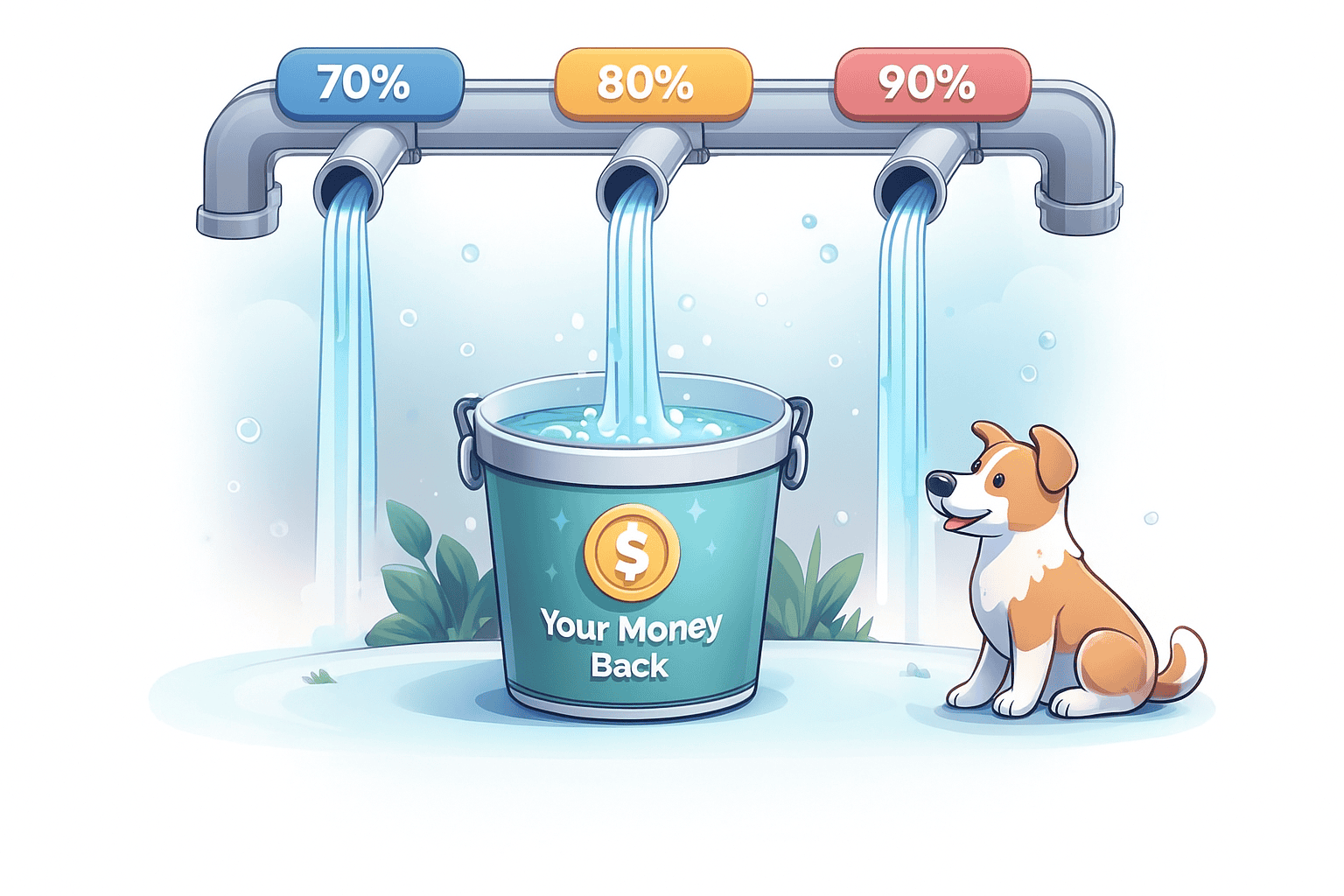

Step 4: Compare Reimbursement Rates

Reimbursement rates decide how much money flows back to you after paying the vet.

Options usually include:

- 70%

- 80%

- 90%

Visualize reimbursement like water returning through a pipe:

- 70% = slow stream

- 80% = steady stream

- 90% = fast stream

Imagine paying a vet bill of $1,000 (₹83,000).

An 80% reimbursement returns 80% of that after your deductible.

This balance directly affects your comfort during emergencies.

Step 5: Read the Exclusions Clearly

Every plan has invisible walls. These walls block certain claims, even if everything else looks perfect.

Common exclusions include:

- Pre-existing conditions

- Breed-based hereditary issues

- Dental diseases

- Behavioral problems

- Injuries or illnesses during waiting periods

- Bilateral issues (both legs, both hips)

Most pet owners only learn about exclusions after a claim is denied.

Reading exclusions now protects you later.

This is where your comparison becomes smarter than 90% of buyers.

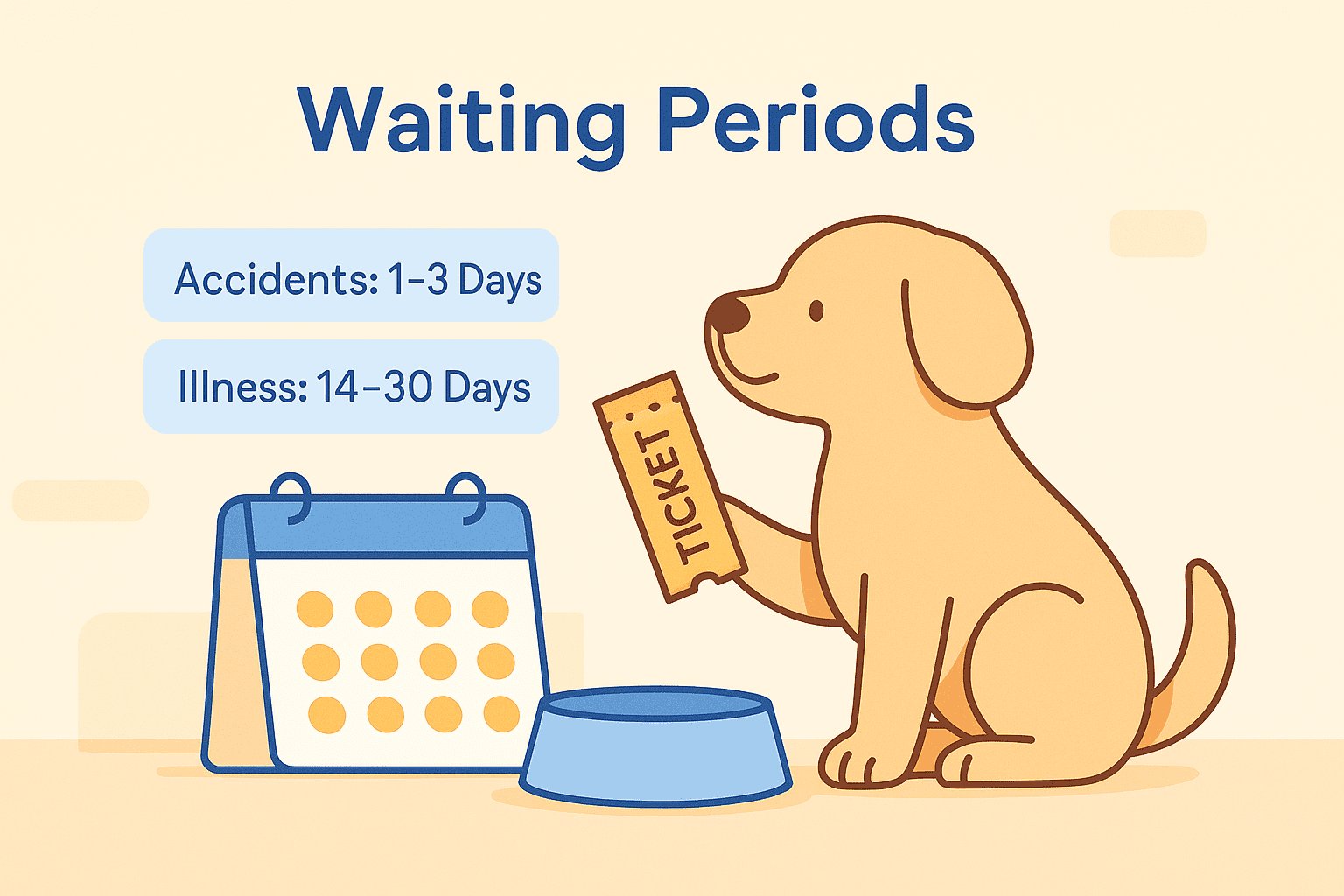

Step 6: Check Waiting Periods

Waiting periods are the quiet days before the policy starts protecting you.

Typical timelines:

- Accidents → 1–3 days

- Illness → 14–30 days

- Ligaments/hips → 6–12 months

Think of the waiting period like buying a movie ticket today, but the movie starts next week.

The ticket is valid.

But you must wait.

Buying insurance early helps avoid trouble later.

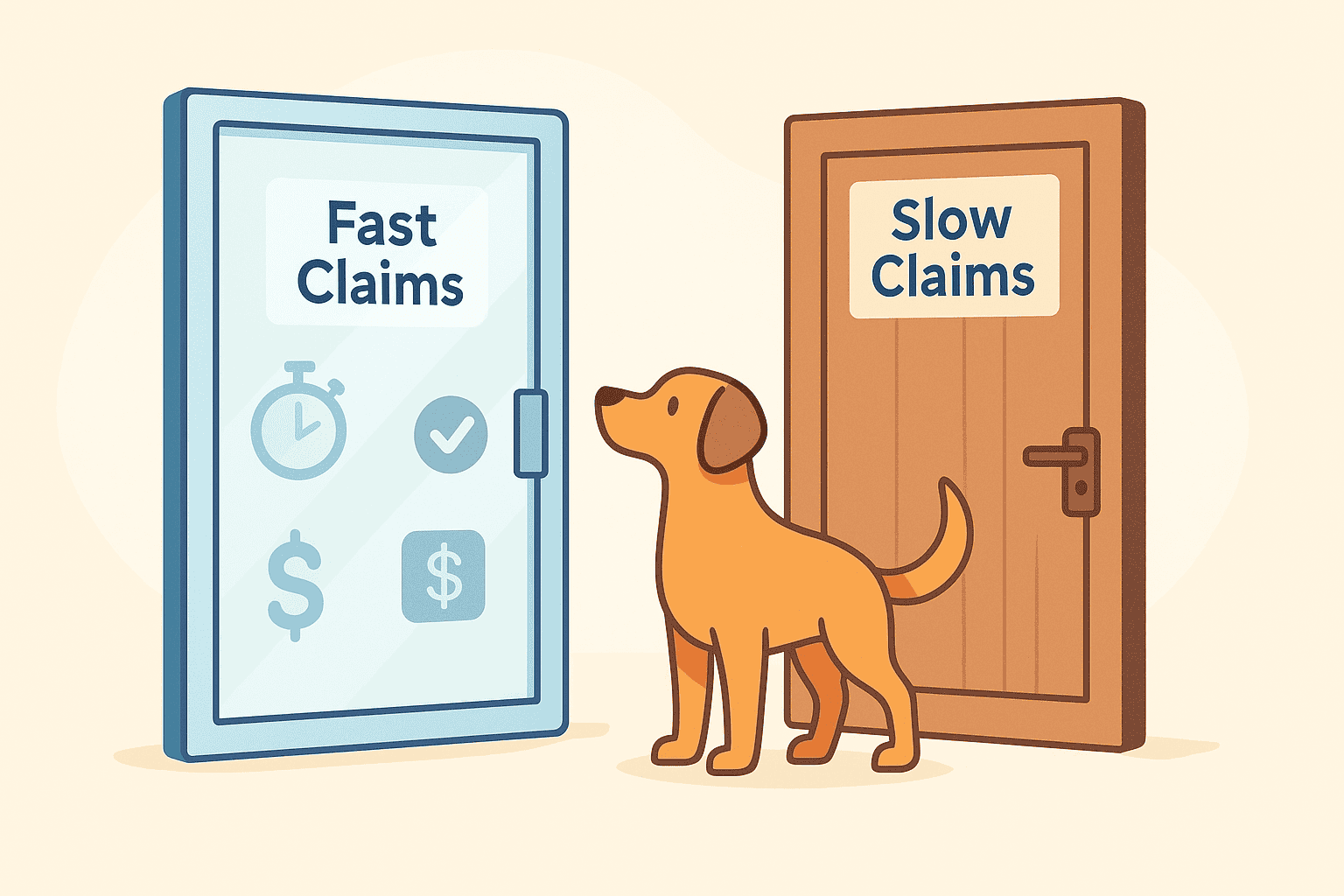

Step 7: Compare Claim Experience

A plan shows its true nature when you file a claim—never before.

Different companies behave differently:

- Some open their doors smoothly.

- Some make the door heavy, slow, and noisy.

When comparing, notice:

- How fast claims are paid

- Whether the app is easy to use

- Whether reimbursements come via direct deposit

- Whether customers praise or complain about delays

- How clear the company is about documentation

A smooth claim experience matters more than a long list of benefits.

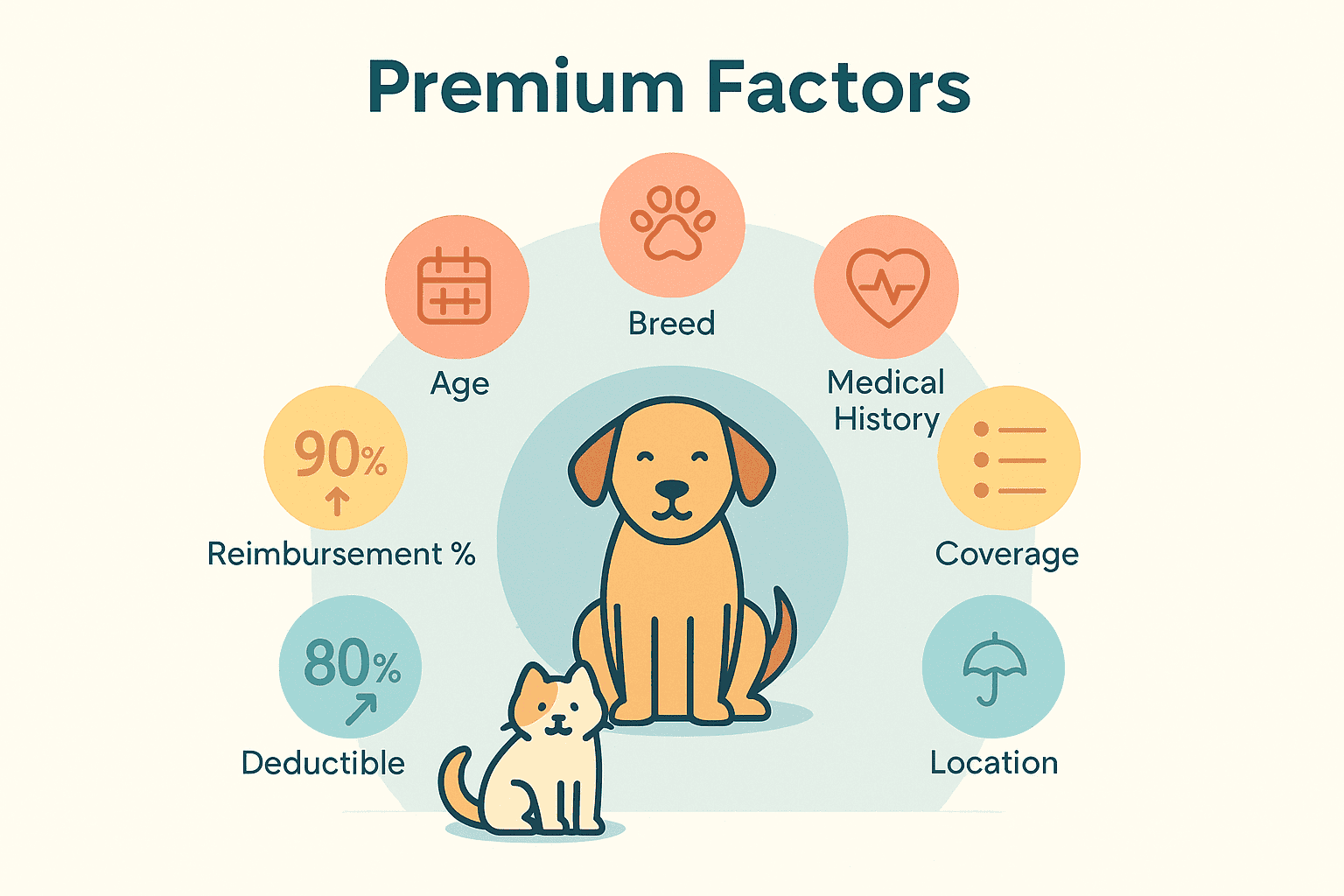

Step 8: Understand Premium Factors

Premiums rise and fall based on your pet’s “risk profile.”

Insurers study patterns like:

- Breed (flat-faced breeds cost more)

- Age (older pets = higher medical risk)

- Zip code (urban vet clinics cost more)

- Coverage limit selected

- Deductible chosen

- Reimbursement rate

- Claim history

A young mixed-breed dog may cost $25 (₹2,075) a month.

A senior French Bulldog may cost $75 (₹6,225) or more.

Understanding this helps you compare plans with realistic expectations instead of assumptions.

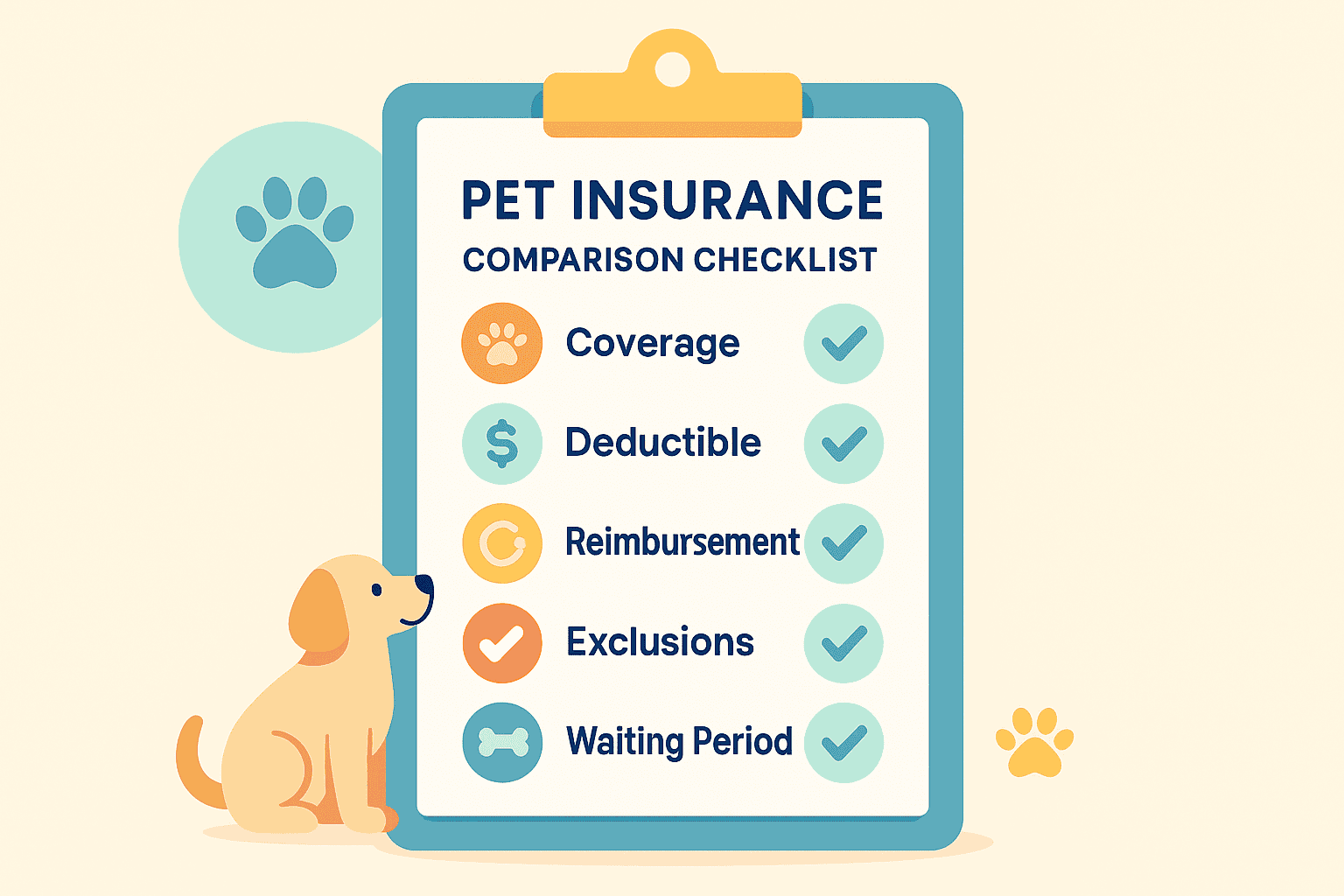

Step 9: Use This Quick Comparison Checklist

Here is a simple checklist that saves you time and confusion:

- What type of plan is this?

- What is the yearly limit?

- What deductible feels right to you?

- What reimbursement rate matches your comfort?

- What exclusions matter to you?

- How long are waiting periods?

- Does the plan cover hereditary problems?

- What do real customers say about claims?

This checklist fits perfectly with long-tail keywords like:

pet insurance comparison checklist

what to check before buying pet insurance online

Step 10: Choose the Right Plan Confidently

By the time you reach this last step, the comparisons feel lighter.

The confusion fades.

You now understand the “shape” of each plan.

The right plan is the one that:

- Protects your pet’s real risks

- Matches your financial comfort level

- Covers both big and small emergencies

- Gives clear terms

- Pays quickly and transparently

- Feels like a safety net rather than a gamble

When you choose confidently, you also care confidently.

FAQs

1. What is the simplest way to compare pet insurance plans online?

Check annual limits, deductibles, reimbursements, exclusions, waiting periods, and claim experiences.

2. Is accident-only coverage enough?

It covers injuries but not illness. Good for young, low-risk pets.

3. Why do premiums increase every year?

Pets age, risk increases, and vet prices rise.

4. Are dental problems covered?

Most plans cover dental injuries, but many exclude dental disease.

5. What yearly limit should you choose?

High-risk breeds → $10,000 (₹8,30,000) or unlimited

Low-risk pets → $5,000 (₹4,15,000) usually works